Page 14 - Demo

P. 14

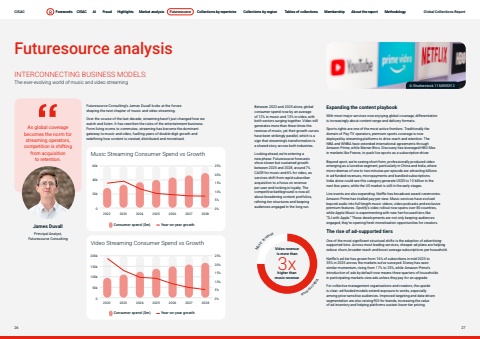

Page titleStandfirstBodyFuturesource analysisINTERCONNECTING BUSINESS MODELS: The ever-evolving world of music and video streamingAs global coverage becomes the norm for streaming operators, competition is shifting from acquisition to retention. James DuvallPrincipal Analyst, Futuresource ConsultingFuturesource Consulting%u2019s James Duvall looks at the forces shaping the next chapter of music and video streaming.Over the course of the last decade, streaming hasn%u2019t just changed how we watch and listen. It has rewritten the rules of the entertainment business. From living rooms to commutes, streaming has become the dominant gateway to music and video, fuelling years of double-digit growth and redefining how content is created, distributed and monetised. Between 2022 and 2025 alone, global consumer spend rose by an average of 12% in music and 13% in video, with both sectors surging together. Video still generates more than three times the revenue of music, yet their growth curves have been strikingly parallel, which is a sign that streaming%u2019s transformation is a shared story across both industries.Looking ahead, we%u2019re entering a new phase. Futuresource forecasts show slower but sustained growth between 2025 and 2028, around 7% CAGR for music and 6% for video, as services shift from rapid subscriber acquisition to a focus on revenue per user and locking in loyalty. The competitive battleground is now all about broadening content portfolios, refining tier structures and keeping audiences engaged in the long run.Music Streaming Consumer Spend vs Growth2022 2023 2024 2025 2026 2027 2028020k40k60k0%5%10%15%20%25%Consumer spend ($m) Year-on-year growthVideo Streaming Consumer Spend vs Growth2022 2023 2024 2025 2026 2027 20280%5%10%15%20%25%Consumer spend ($m) Year-on-year growth050k100k200k150kExpanding the content playbookWith most major services now enjoying global coverage, differentiation is increasingly about content range and delivery formats.Sports rights are one of the most active frontiers. Traditionally the domain of Pay-TV operators, premium sports coverage is now deployed by streaming platforms to drive reach and retention. The NBA and WNBA have extended international agreements through Amazon Prime, while Warner Bros. Discovery has leveraged HBO Max in markets like France, to push live sports as a subscription driver.Beyond sport, we%u2019re seeing short-form, professionally produced video emerging as a lucrative segment, particularly in China and India, where micro-dramas of one to two minutes per episode are attracting billions in ad-funded revenues, micropayments and bundled subscriptions. India alone could see this category generate US$5 to 10 billion in the next few years, while the US market is still in the early stages.Live events are also expanding. Netflix has broadcast award ceremonies. Amazon Prime has trialled pay-per-view. Music services have evolved beyond audio into full-length music videos, video podcasts and exclusive premium features. Spotify%u2019s video rollout now spans over 80 countries, while Apple Music is experimenting with new fan-focused tiers like %u201cDJ with Apple.%u201d These developments are not only keeping audiences engaged, they%u2019re opening fresh monetisation opportunities for creators.The rise of ad-supported tiers One of the most significant structural shifts is the adoption of advertisingsupported tiers. Across most leading services, cheaper ad plans are helping reduce churn, broaden reach and boost average subscriptions per household. Netflix%u2019s ad tier has grown from 16% of subscribers in mid-2023 to 35% in 2025 across the markets we%u2019ve surveyed. Disney has seen similar momentum, rising from 17% to 25%, while Amazon Prime%u2019s introduction of ads by default now means three-quarters of households in participating markets view ads unless they pay for an upgrade. For collective management organisations and creators, the upside is clear: ad-funded models extend exposure to works, especially among price-sensitive audiences. Improved targeting and data-driven segmentation are also raising ROI for brands, increasing the value of ad inventory and helping platforms sustain lower-tier pricing.3x higher than music revenue Video revenue is more thanMusic revenueV di eoervenue%u00a9 Shutterstock 1154935312CISAC Forewords CISAC AI Fraud Highlights Market analysis Futuresource Collections by repertoire Collections by region Tables of collections Membership About the report Methodology26 27Forewords CISAC AI Fraud Highlights Market analysis Futuresource Collections by repertoire Collections by region Tables of collections Membership About the report Methodology Global Collections Report